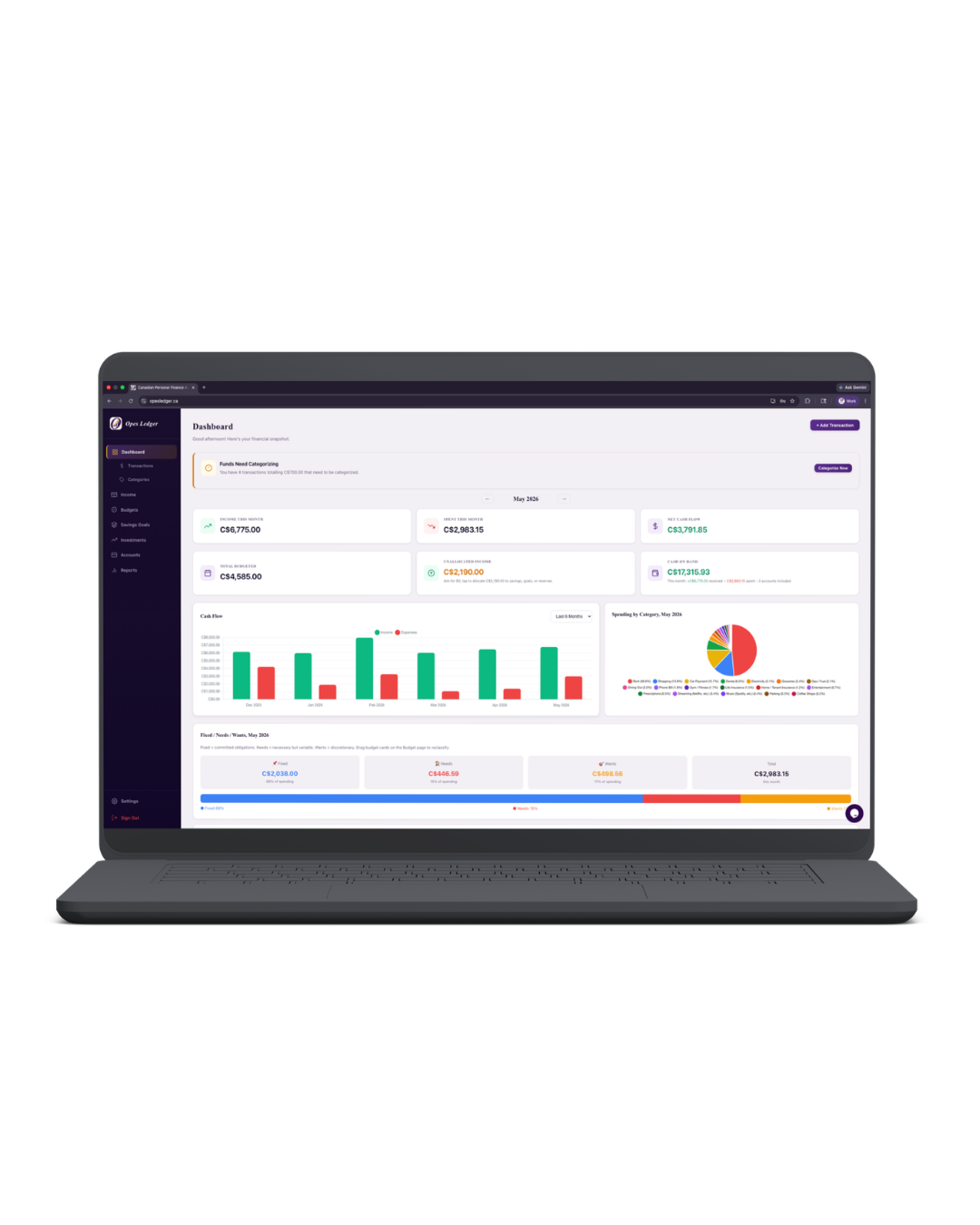

Dashboard

Good morning! Here's your financial snapshot.

Cash Flow

Spending by Category,

Fixed / Needs / Wants,

Fixed = committed obligations. Needs = necessary but variable. Wants = discretionary. Drag budget cards on the Budget page to reclassify.

Needs vs Wants. Monthly Breakdown

How your needs and wants spending has changed over time.

Recent Transactions

See allTransactions

Track every dollar in and out.

| Date | Description | Category | Account | Amount |

|---|

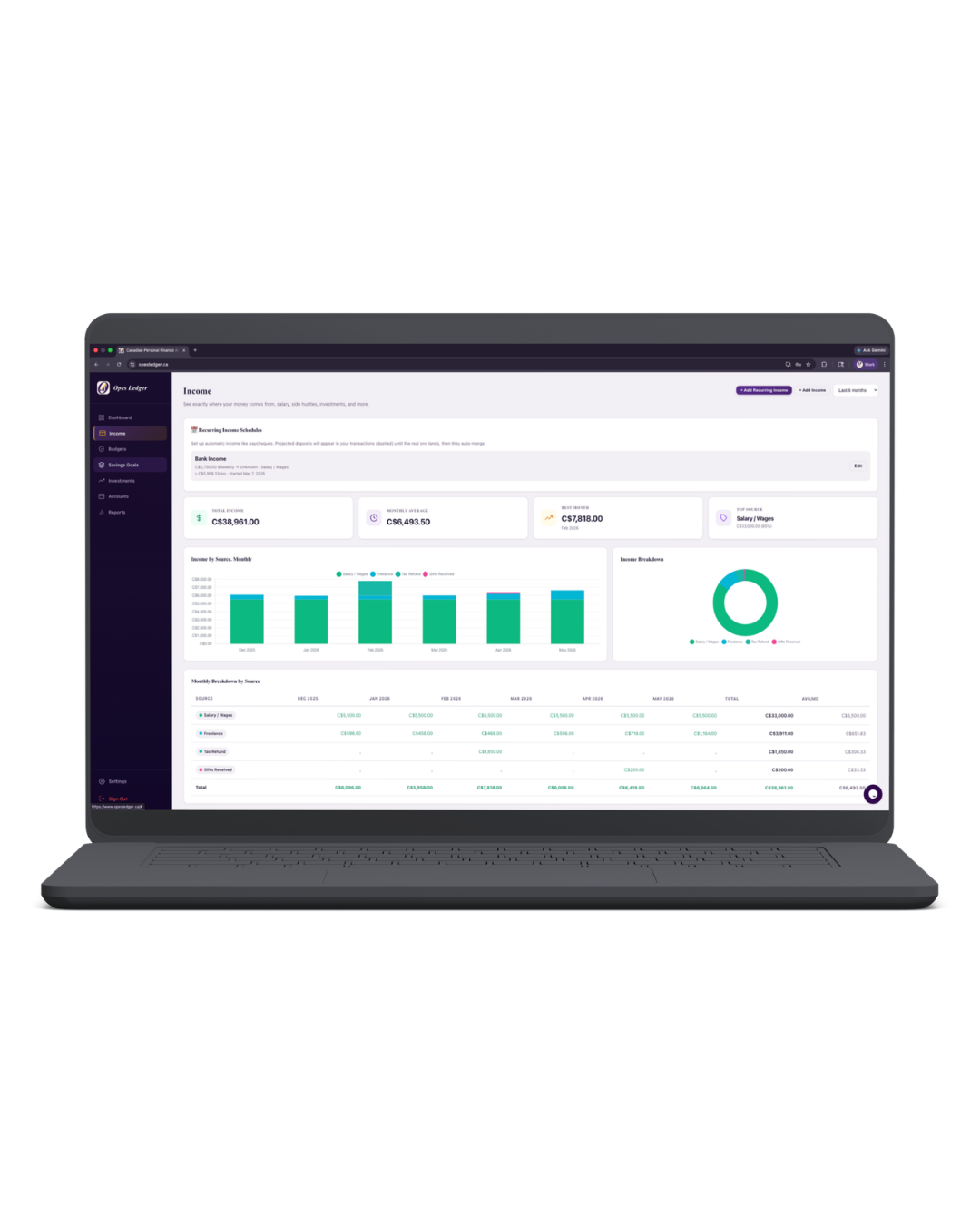

Income

See exactly where your money comes from, salary, side hustles, investments, and more.

Income by Source. Monthly

Income Breakdown

Monthly Breakdown by Source

All Income Transactions

| Date | Description | Source | Account | Amount |

|---|

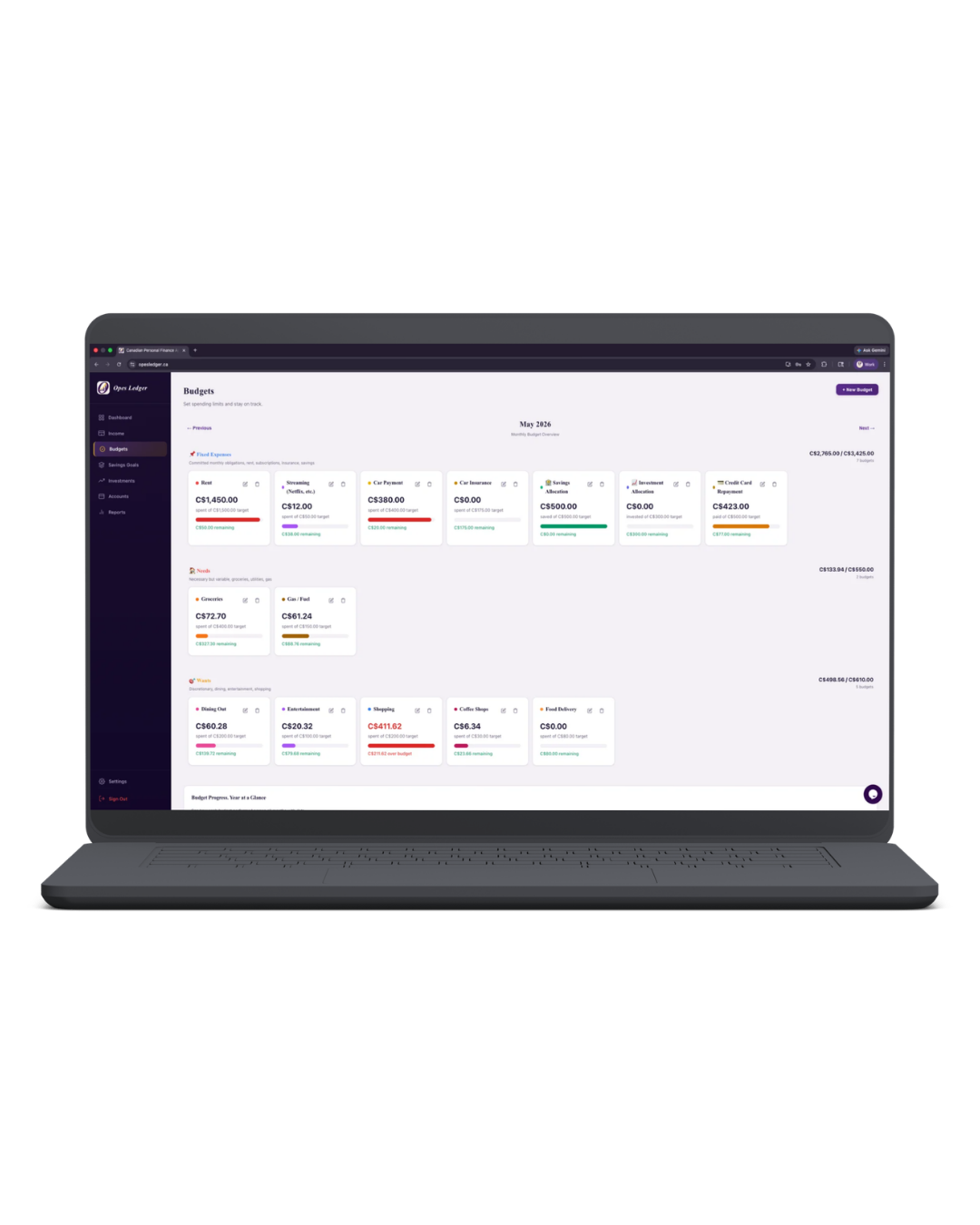

Budgets

Set spending limits and stay on track.

Monthly Budget Overview

Budget Progress. Year at a Glance

See how each budget performed across all months with data.

Savings Goals

Save for what matters to you, vacations, retirement, big purchases, and more.

Investments

Track your portfolio across all platforms.

Portfolio Allocation

By Platform

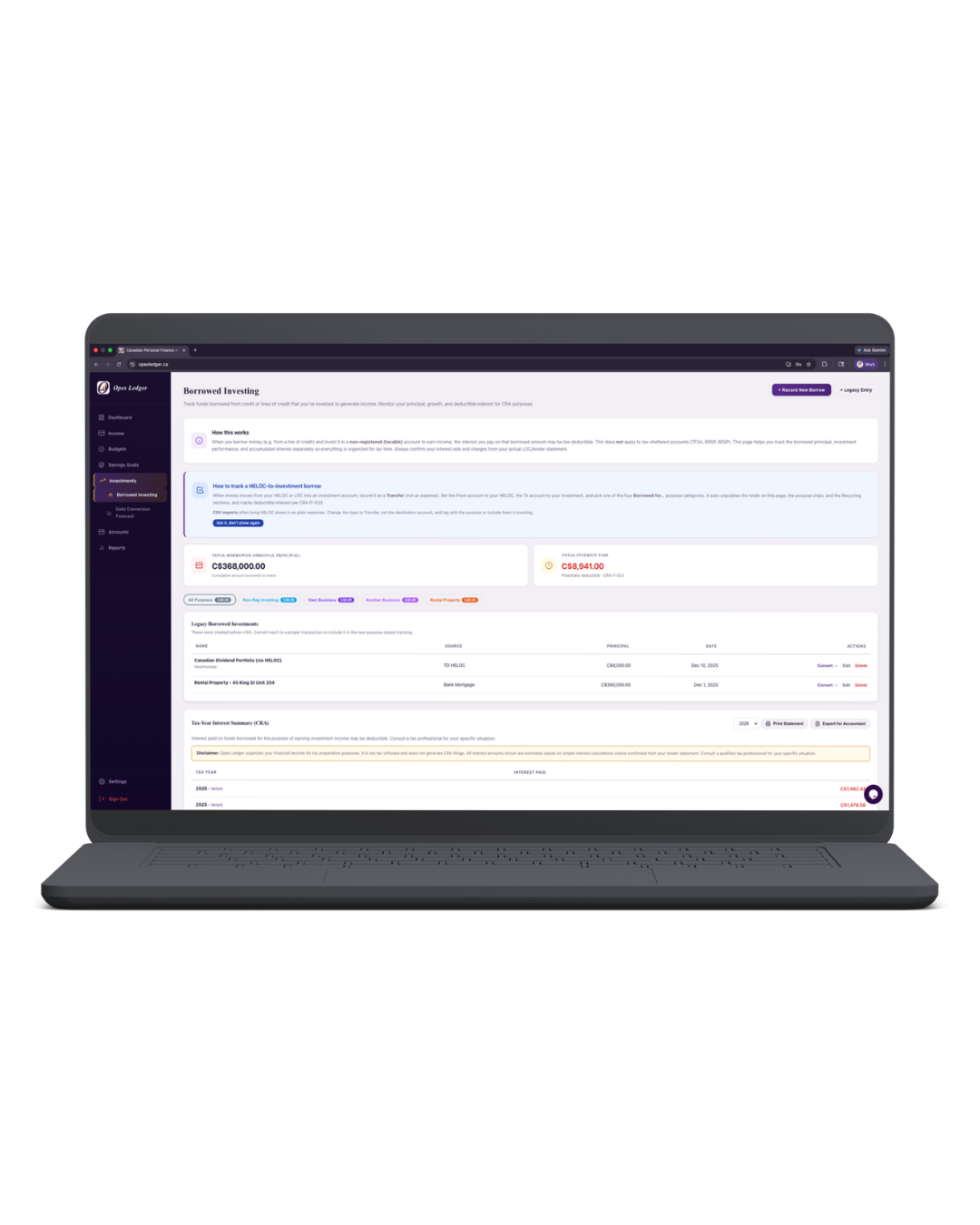

Borrowed Investing

Track funds borrowed from credit or lines of credit that you've invested to generate income. Monitor your principal, growth, and deductible interest for CRA purposes.

When you borrow money (e.g. from a line of credit) and invest it in a non-registered (taxable) account to earn income, the interest you pay on that borrowed amount may be tax-deductible. This does not apply to tax-sheltered accounts (TFSA, RRSP, RESP). This page helps you track the borrowed principal, investment performance, and accumulated interest separately so everything is organized for tax time. Always confirm your interest rate and charges from your actual LOC/lender statement.

Tax-Year Interest Summary (CRA)

Interest paid on funds borrowed for the purpose of earning investment income may be deductible. Consult a tax professional for your specific situation.

Scenario Calculator

Read-only, does not modify your dataExplore "what if" scenarios before committing. Enter hypothetical numbers to see projected interest costs, tax savings, and breakeven returns.

This calculator is for illustrative purposes only. Actual results depend on your specific tax situation, investment returns, and lender terms. This is not financial advice.

Interest Deduction. How It Works

When you borrow money to earn investment income (dividends, rental income, interest, etc.), the interest you pay on those borrowed funds may be tax-deductible on your Canadian tax return (Line 22100).

What your accountant will need:

- Your annual interest paid on borrowed funds (tracked above)

- Proof that borrowed funds were used to earn income

- Your LOC or credit card statements showing interest charges

- Records of income earned from those investments

How the deduction is calculated: Your accountant applies the deductible interest against your pre-tax income using your marginal tax rate (federal + provincial combined). The actual savings depend on your total taxable income, province, and individual tax situation.

Tip: Use the "Print Annual Statement" button above to generate a document you can give to your accountant. It includes all the interest and income details they need, organized by CRA guidelines (IT-533).

Debt Conversion Recycling

Convert non-deductible primary-residence mortgage debt into potentially tax-deductible investment debt. Cycle: Income → Mortgage Prepayment → HELOC Reborrow → Non-Registered Investment. Interest on HELOC funds used to earn investment income may be deductible (CRA IT-533).

Mortgage Prepayment History

| # | Date | From Account | Prepayment Amount | Cumulative Prepaid | HELOC Room Created | Applied to Mortgage | Description |

|---|

HELOC Reborrows → Investment

Auto-populated from transactions| # | Date | Description | Amount | HELOC Rate | Monthly Interest | Accrued to Date | Cumulative Reborrowed | Account |

|---|

Deductible Interest Summary

HELOC interest on funds reborrowed and invested in non-registered income-producing assets may be deductible on Line 22100. Keep clear documentation of the direct-use trace for CRA.

Disclaimer: Opes Ledger organizes your financial records for tax preparation purposes. It is not tax software. Consult a qualified tax professional.

Business Debt Conversion (Primary Residence)

Track the cycle: Business Income → Mortgage Prepayment → HELOC Reborrow → Back to Business. HELOC interest may be tax-deductible when funds are used for business purposes.

Rental Income Debt Conversion

Track the cycle: Rental Income → Mortgage Prepayment → HELOC Reborrow → Rental Property Investment. HELOC interest may be tax-deductible when borrowed funds are used to earn rental income.

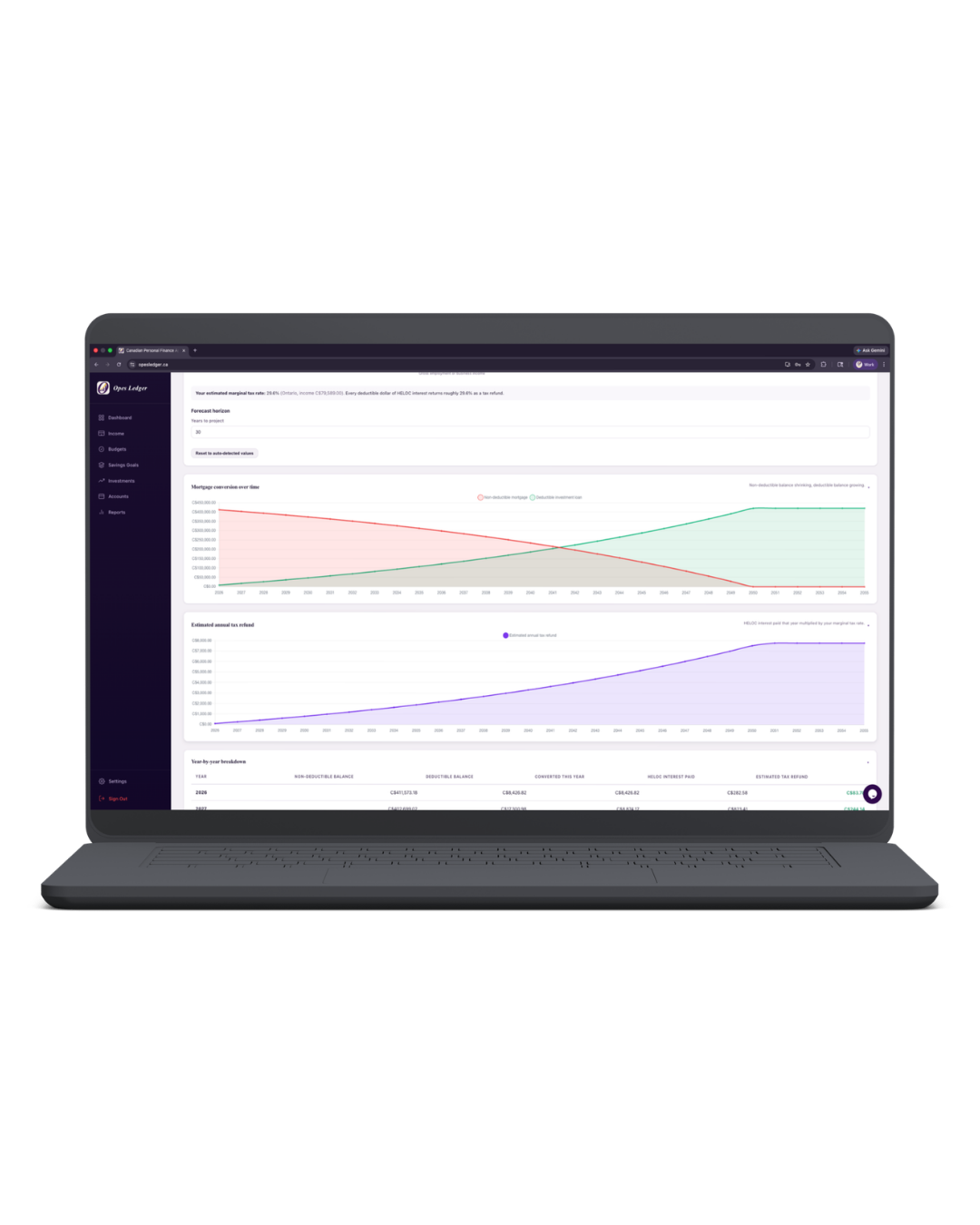

Debt Conversion Forecast

Your personal Mortgage to Millions breakdown. See how fast you are converting non-deductible mortgage debt into tax-deductible investment loans, and the estimated annual tax refunds over time.

Assumptions

Use "Planning a future mortgage" to see the forecast for a purchase you have not closed on yet. Once you have the actual mortgage, switch to "Existing mortgage" and the forecast will use your real account data.

Mortgage details

Conversion strategy

Beyond your regular mortgage principal, you can layer additional monthly prepayments from different income sources. Each source corresponds to a different CRA tax treatment when you reborrow. In couple mode, use the "Who claims" dropdown to attribute each source to the right partner.

Your tax profile

Forecast horizon

Mortgage conversion over time

Estimated annual tax refund

Year-by-year breakdown

▾| Year | Non-deductible balance | Deductible balance | Converted this year | HELOC interest paid | Estimated tax refund |

|---|

Interest accumulated by source

▸See how much deductible HELOC interest comes from each source, per month and per year, so you can match the numbers to the right CRA form at tax time.

Investment growth projection

▸Project the future value of the reborrowed funds you invest each month. The whole point of debt conversion is to take advantage of compound growth, like a self-directed retirement plan.

Disclaimer. This forecast uses your current data and assumed rates to project a possible path. Actual results will vary based on conversion consistency, interest rate changes, investment performance, and CRA compliance. This tool organizes information for planning purposes and is not tax, legal, or investment advice. Always consult a qualified Canadian mortgage broker, accountant, or financial advisor before making decisions. If you would like a referral, email hello@opesledger.ca.

Accounts

All your money in one place.

Total of All Accounts Over Time

Credit Cards

Track balances, charges, payments, and due dates for all your credit cards.

Lines of Credit

Track balances, draws, repayments, and interest on your personal LOC and HELOC.

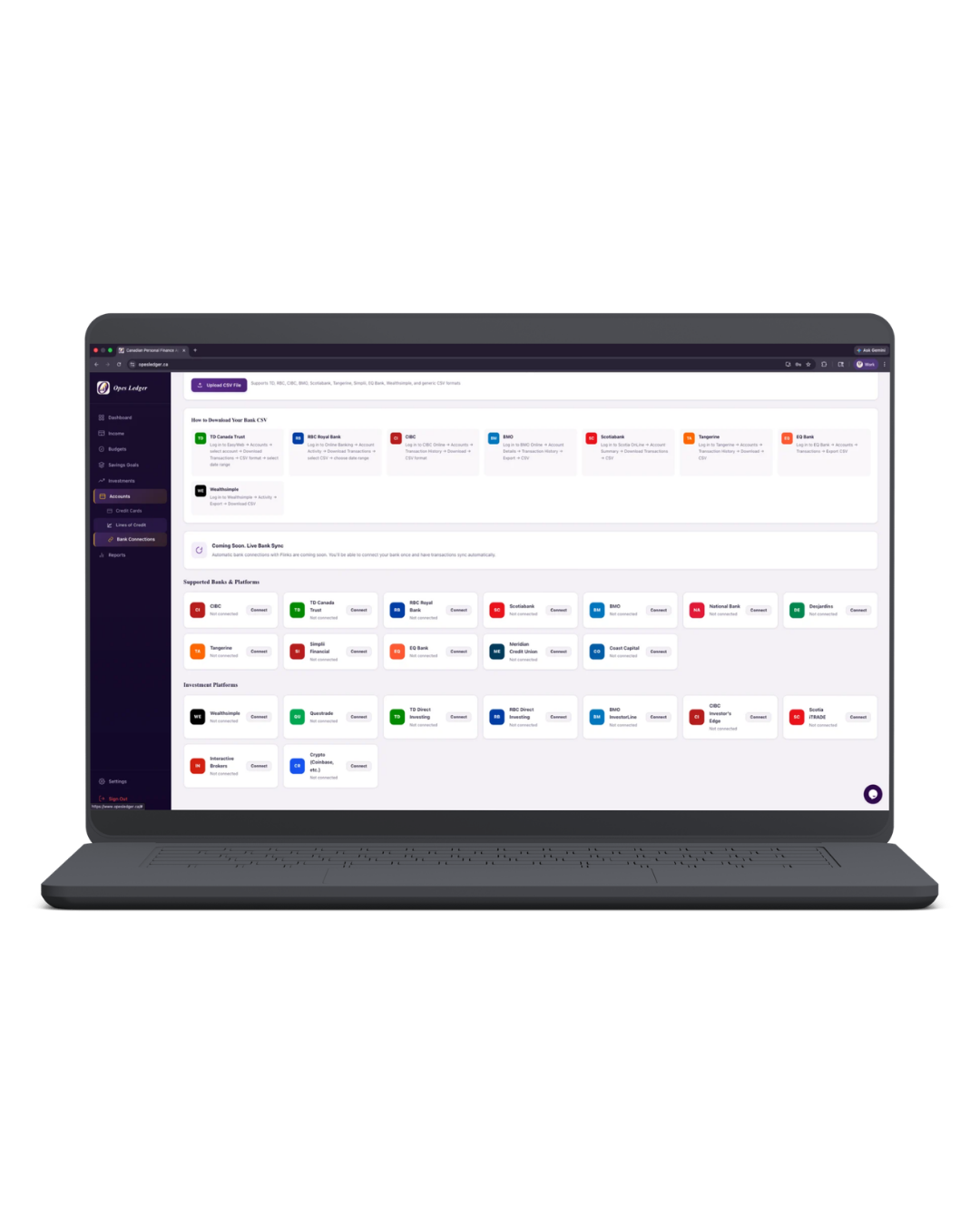

Bank Connections

Import transactions from your Canadian bank or connect accounts.

Import Bank Transactions (CSV)

Download your transaction history as a CSV file from your bank's online banking, then upload it here. We'll auto-detect the format.

How to Download Your Bank CSV

Automatic bank connections with Flinks are coming soon. You'll be able to connect your bank once and have transactions sync automatically.

Supported Banks & Platforms

Investment Platforms

Categories

Create and manage your spending and income categories.

Needs

Essential expenses, housing, utilities, groceries, insurance, transport.

Wants

Non-essential expenses, dining out, entertainment, subscriptions, shopping.

Income

Categories for tracking where your money comes from.

Auto-Categorize

Set up rules so transactions are automatically categorized. When a transaction description matches a keyword, it gets assigned the right category instantly.

When you add a transaction (or one comes in from a bank connection), the description is checked against your rules. If it matches a keyword, the category is auto-filled. Rules are also learned from your past transactions, categorize something once, and it remembers for next time.

Learned from History

These were automatically learned from your past transactions. When you categorize a transaction, it remembers the description for next time.

Custom Rules

Rules you've created manually. Keywords are matched against transaction descriptions (case-insensitive). You can use multiple keywords separated by commas.

Bulk Re-Categorize

Apply all rules to your existing transactions. This will update any uncategorized or mis-categorized transactions that match your rules.

Reports

Understand your spending habits.

Extra Cash Remaining,

Income minus expenses per month. Positive = surplus, negative = overspend.Emergency Income Floor

Minimum income to cover your Fixed obligations. Use this to size your emergency fund.Income by Month. Year Comparison

Expenses by Month. Year Comparison

Spending by Category. Year Comparison

Top 5 Spending Categories, 2026

Category Breakdown

Settings

Customize your experience.

Currency

Choose your display currency.

Appearance

Switch between light and dark mode.

Data

Export or reset your data.

Load Sample Data

Populate the app with realistic example data to explore all features.

Subscription

Your current plan and billing.

Account

Permanently close your account. This cancels your subscription, deletes all your data, and removes your login. This cannot be undone.

Install App

Install Opes Ledger on your device for quick access and offline support.

Report a Bug

Found something that doesn't look right? Let us know and we'll fix it.